Seven years after the global financial crisis erupted in 2008, the world economy continued to stumble in 2015. According to the United Nations’ report World Economic Situation and Prospects 2016, the average growth rate in developed economies has declined by more than 54% since the crisis. An estimated 44 million people are unemployed in developed countries, about 12 million more than in 2007, while inflation has reached its lowest level since the crisis.

More worryingly, advanced countries’ growth rates have also become more volatile. This is surprising, because, as developed economies with fully open capital accounts, they should have benefited from the free flow of capital and international risk sharing – and thus experienced little macroeconomic volatility. Furthermore, social transfers, including unemployment benefits, should have allowed households to stabilise their consumption.

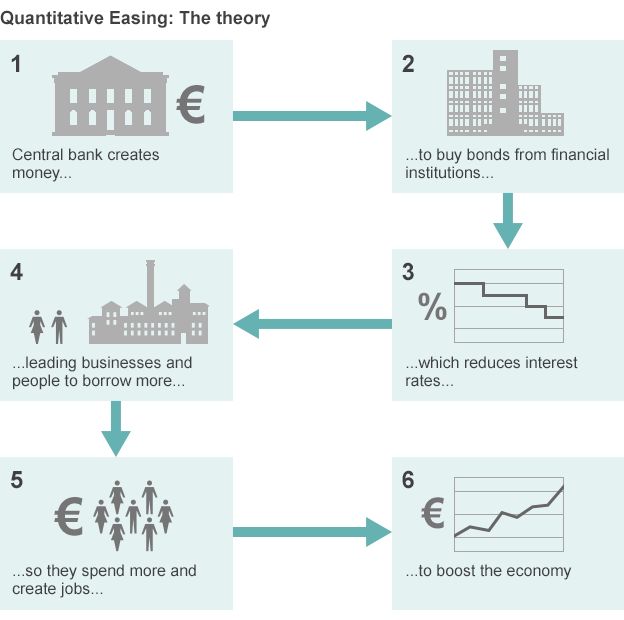

But the dominant policies during the post-crisis period – fiscal retrenchment and quantitative easing (QE) by major central banks – have offered little support to stimulate household consumption, investment, and growth. On the contrary, they have tended to make matters worse.

In the US, quantitative easing did not boost consumption and investment partly because most of the additional liquidity returned to central banks’ coffers in the form of excess reserves. The Financial Services Regulatory Relief Act of 2006, which authorised the Federal Reserve to pay interest on required and excess reserves, thus undermined the key objective of QE...

No comments:

Post a Comment